dido:public:ra:xapend:xapend.a_glossary:c:clearing_house

Differences

This shows you the differences between two versions of the page.

| Both sides previous revision Previous revision Next revision | Previous revision | ||

|

dido:public:ra:xapend:xapend.a_glossary:c:clearing_house [2022/04/25 20:42] nick |

dido:public:ra:xapend:xapend.a_glossary:c:clearing_house [2022/04/25 21:01] (current) nick |

||

|---|---|---|---|

| Line 4: | Line 4: | ||

| **Clearinghouse** is a designated intermediary between a buyer and seller in a [[dido:public:ra:xapend:xapend.a_glossary:f:financial_market]]. The **Clearinghouse** validates and finalizes the transaction, ensuring that both the buyer and the seller honor their contractual obligations. | **Clearinghouse** is a designated intermediary between a buyer and seller in a [[dido:public:ra:xapend:xapend.a_glossary:f:financial_market]]. The **Clearinghouse** validates and finalizes the transaction, ensuring that both the buyer and the seller honor their contractual obligations. | ||

| - | Every Financial Market has a designated https://www.investopedia.com/terms/c/clearinghouse.asp or an internal clearing division to handle this function. | + | Every Financial Market has a designated **Clearinghouse** or an internal clearing division to handle this function. |

| The responsibilities of a **Clearinghouse** include "clearing" or finalizing trades, settling trading accounts, collecting margin payments, regulating delivery of the assets to their new owners, and reporting trading data. | The responsibilities of a **Clearinghouse** include "clearing" or finalizing trades, settling trading accounts, collecting margin payments, regulating delivery of the assets to their new owners, and reporting trading data. | ||

| Line 11: | Line 11: | ||

| In order to act efficiently, a **Clearinghouse** takes the opposite position of each trade, which greatly reduces the cost and risk of settling multiple transactions among multiple parties. While their mandate is to reduce risk, the fact that they have to act as both buyer and seller at the inception of a trade means that they are subject to default risk from both parties. To mitigate this, clearinghouses impose margin requirements. | In order to act efficiently, a **Clearinghouse** takes the opposite position of each trade, which greatly reduces the cost and risk of settling multiple transactions among multiple parties. While their mandate is to reduce risk, the fact that they have to act as both buyer and seller at the inception of a trade means that they are subject to default risk from both parties. To mitigate this, clearinghouses impose margin requirements. | ||

| + | |||

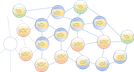

| + | <figure clearingHouse> | ||

| + | {{ :dido:public:ra:xapend:xapend.a_glossary:c:screen_shot_2022-04-25_at_5.55.31_pm.png?500 |}} | ||

| + | <caption>The relationship between a buyer, a seller and a Clearinghouse.</caption | ||

| + | </figure> | ||

dido/public/ra/xapend/xapend.a_glossary/c/clearing_house.1650933746.txt.gz · Last modified: 2022/04/25 20:42 by nick